Demand-Driven Assets: Swivel's Role

This article follows the article “Demand Driven Assets” and is the second in a series by Swivel on our vision for the future of digital assets.

In the previous article we discussed how investors and capital seekers are currently joined via standardized instruments traded in intermediated markets. We described the promise of digital securities to provide a more precise and direct matching between investor and capital markets. We further showed the benefit of creating securities that can be decomposed into component cash flows which in turn may be applied to create bespoke structured products with little to no overhead. We closed with a summary of the building blocks necessary to deliver such a solution.

TL;DR

This article assesses the previously described demand-driven asset model in the context of Swivel’s current platform. Swivel enables the generation of assets in response to known demand, rather than the preemptive generation of assets and then seeking of buyers. Further, Swivel provides opportunities to bring new assets based on decomposed cash flows to the market and supports various optimization instruments.

The three-way tie

In simplest terms, all investors seek to optimize three dimensions:

Return

Level of risk

Period of time

As digital asset issuance continues to become faster, cheaper and more efficient, assets can be created directly from investor demand according to their personal risk/return tolerance and time window. This is unlike traditional wholesale capital markets which first create instruments and then seek buyers. Buyers can now specify the time, risk and return dimensions of the assets they want and have issuers match their needs. No asset is created unless the demand exists.

Swivel’s product delivers on this vision of spontaneously generating new instruments at the intersection of two or more participants’ corresponding needs. Further, decomposing these assets into their underlying cash flows can support even more precise matching of supply and demand, particularly when time is considered.

Swivel directly facilitates the ability to manage risk by allowing users to trade predictable cash flows (fixed-rate) via receiving tokenized zero-coupon bonds or the ability to leverage capital exposure by purchasing interest coupons.

Investors seeking stable returns have the ability to create orders on our order book for a desired amount of principal, as well as rate sought and desired maturity date. Maturity dates are synchronized to support fungible positions and assure an orderly market with straightforward dates against which returns can be compared on a like for like basis.

Interest rate speculators fill the order, paying an upfront premium equal to the rate sought, and in return receive a time-locked vault of the tendered principal which is then provided to money-markets in order to generate interest. Note that this model means that on-chain costs (in the form of gas) are expended only as and when a new asset is matched to a buyer, significantly reducing the cost for issuers. If no buyer for an asset is found, no assets are minted and the issuer bears no cost.. Furthermore, the lender is insulated from counterparty risk because the premium must be paid upfront or the transaction does not occur,

Investor demand is expressed as an order. As the order is filled, investors exchange cash flows and obligations for rights that exactly fulfill their investor needs. The set of tokens representing the filled order’s cash flows are only created when the match is found.

Unlike a more traditional model where a generic, standardized asset is first created then brought to market, demand for a new asset is found using the order book as a discovery mechanism. Swivel currently matches investors across a single transaction type, the exchange of fixed or floating interest rates. The instruments created are a vault contract containing “Notional Tokens” (representing the total value of the interest payments on the floating side) and the “Zero-Coupon Bond Token” (representing the return of principal to the lender at the end of the period).

The initial version of the product is simple, with a limited number of moving pieces to isolate risk and enable timely delivery. But the order book mechanism that allows this matching of investor and capital seeker can serve as a factory for a variety of cash-flow-based instruments.

Breaking it down

In the previous article in this series, we talked about Alice and her need to borrow money, repayable in one year at a fixed rate of interest. We discussed how traditional markets would treat this agreement as a single unit, and how a future model using tokenized obligations representing each interest coupon could help Alice find the investors she needs while also offering the specific maturity dates each investor seeks.

Let’s look at how this future model can be executed using Swivel.

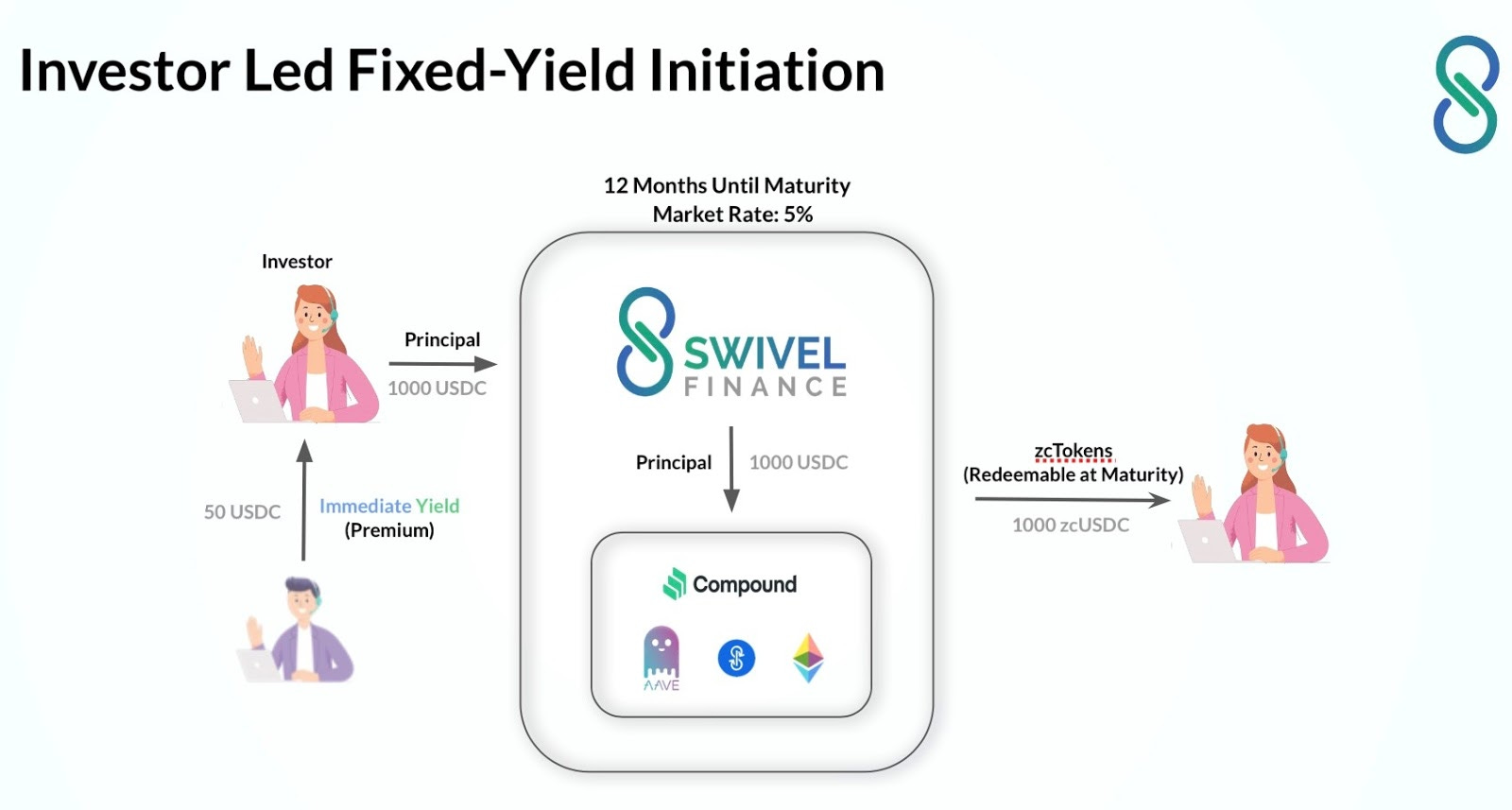

Assume Alice has $1000 in principal she wishes to lend at a fixed rate. She places an order via Swivel, seeking a five percent interest premium. Bob, an investor seeking $1000 at no more than five percent, fills the order. When this agreement occurs Swivel creates three new assets:

A premium payment representing the fixed interest immediately payable to Alice

A zero coupon token representing Alice's principal loaned to Bob which is redeemable 1-1 for principal upon maturity.

A notional token representing the floating rate interest payable to Bob.

This current-version example illustrates a single balloon repayment to Alice at the end of the period, so there’s only one zero coupon token.

Individual Cash Flow Tokens

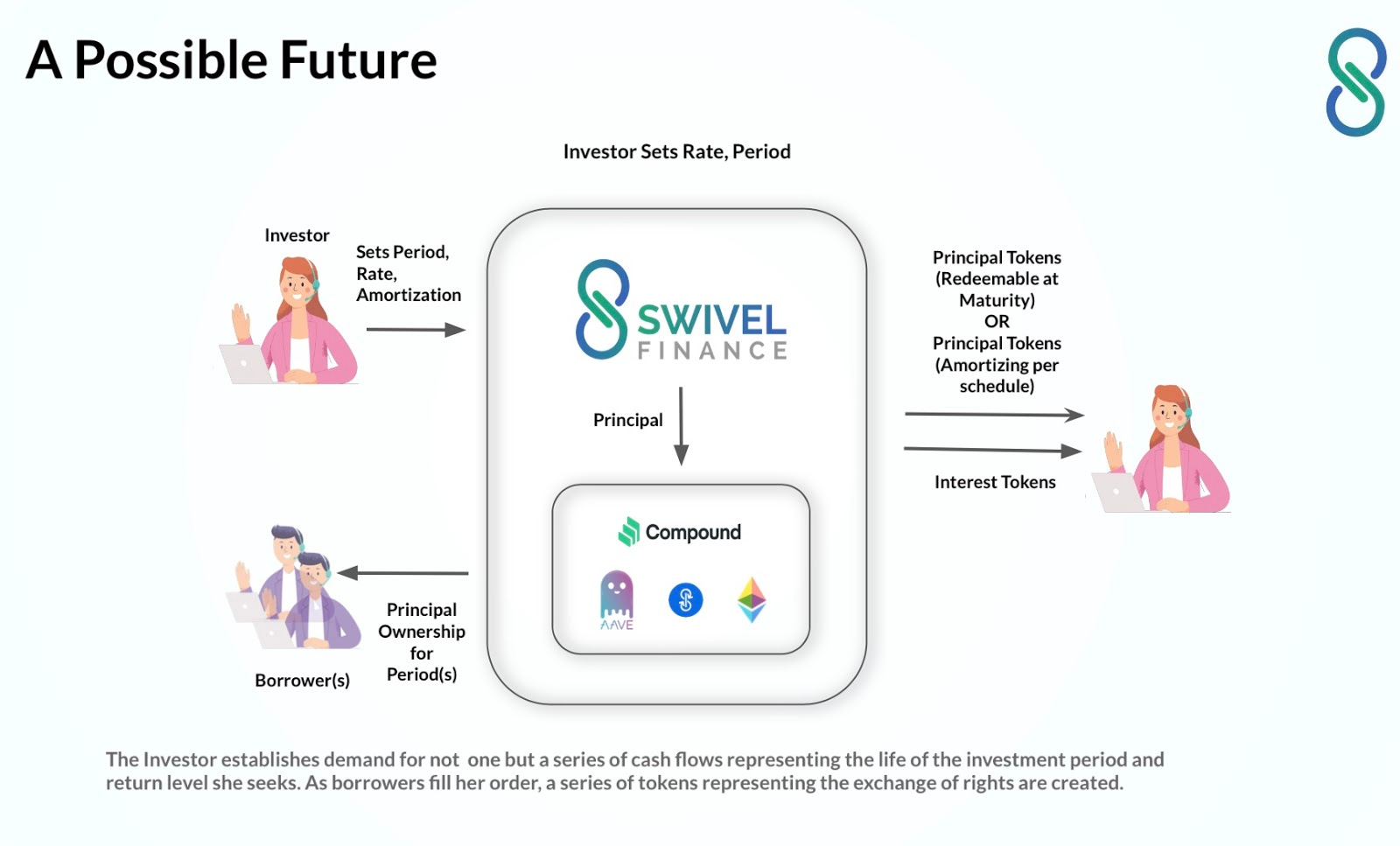

But let’s imagine Alice’s loan was amortizing, with twelve monthly principal repayments due from Bob.

Alice could generate not one zero coupon token, but a series of twelve tokens representing each of the monthly principal repayments. Likewise the fixed rate premium from Bob could also be split into twelve tokens due to Alice over the life of the agreement. If Bob only wanted to borrow for three months, he could fill an order for those months, and receive only the specific duration of exposure he needs. Other parties could fill the pieces of the order that met their needs, and only when the order is completely filled would it be executed and the tokens created. Both Alice and Bob are then guaranteed that their expressed demand is met, and when it is not, are insulated from partial execution risk.

In a simple, small transaction for limited duration like the one-year exchange of $1000 at fixed-for-floating terms, this multiple token scenario may be of limited value.

But in a marketplace for much larger ticket sizes spread over a wider range of maturities, breaking the transaction into specific cash flows becomes a highly useful tool in matching the needs of an individual or multiple borrowers with an array of potential investors whose individual or combined portfolio or hedging needs create a perfect fit.

The ability to break down the transaction into much smaller pieces of limited duration also has the potential to democratize access to cash flows and promote financial inclusion. Smaller investors can participate in rate optimization markets while securing access to wholesale pricing from the large-ticket deal on the other side. Individuals and small businesses seeking rate optimization now have an opportunity previously available only to large corporations and financial institutions.

Building the scaffolding for decentralized finance

As the infrastructure to make the increasingly seamless match of investor demand to capital seekers’ needs continues to evolve, we can foresee a future marketplace where many of the intermediate functions devolve from institutions into software.

Just as new assets may be generated to meet specific needs on the fly, these new simple assets can, over time, be extended. They may maintain their own registry of ownership and obligations. Governed by the market’s self-generated transactional rules, the assets themselves can generate new cash flows and distribute them to the correct entitled parties. Digital securities become their own back office.

Swivel’s current capital efficient issuance and order book mechanisms provide the initial capability to exchange fixed for floating rate positions. In the near future, we will enable the efficient management of a variety of programmable cash-flows. These programmable cash-flows then enable various structured instruments that become core to next-generation efficient capital allocation and risk management. Further, we anticipate providing instruments to manage the differences in risk and maturity dates across different cash instruments, enabling more accurate hedging and improved fungibility.

—Clark Thompson, Business Development and Strategy Lead

Website | Substack | Discord | Twitter | Github | Gitcoin | Careers